Welcome to WordPress. This is your first post. Edit or delete it, then start writing!

Hello world!

October 22, 2019

|In Uncategorised

Private equity has traditionally been an exclusive asset class only available to the “big end of town” and the ultra-wealthy. But, increasingly, everyday investors, including self-managed superannuation funds, are being given the chance to hop on the global private equity bandwagon.

Private equity’s popularity has grown due to several favourable characteristics, such as its historical performance across economic cycles. It allows for value creation and long-term investment horizons, as it typically doesn’t experience the same short-term fluctuations as listed equities. It also brings an “illiquidity premium” from the nature of the underlying companies, which is attractive to investors over the longer term.

More than 70% of large institutional investors allocate funds to private equity, with the average target being about 14%. Australia’s Future Fund, for example, allocates about 16.8% of its portfolio to private equity.

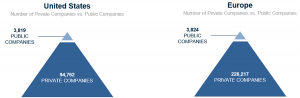

The growth of private companies has corresponded with a decline in publicly listed companies: for example, in 2000 there were 8090 listed US companies, yet by early 2022 this had more than halved to 3819.

Private equity provides the opportunity for inves- tors to vastly expand their universe of investable companies. Compared with those 3819 listed compa- nies in the US, there are 94,762 private companies. In Europe, there are 3824 listed developed market com- panies compared with 226,217 private companies.

Investors who only put their savings in listed companies are effectively restricting themselves to just 2% of companies in the world.

Investing in private equity can take several forms. In Australia, investors tend to (incorrectly) associate private equity investing purely with venture capital – providing capital for start-ups. Yet venture capital is only one small part of many private equity strategies.

There is a private equity spectrum, from “angel investing” (providing very early seed money to start- ups) right through to distressed funding (buying the debt or assets of a distressed business and trying to return it to profitability).

But by far the most common private equity invest- ment strategies sit somewhere in between: through either buyouts or growth equity.

Buyouts are the most common private equity strategy, through either acquiring a controlling posi- tion in larger, more mature companies with estab- lished cashflows. Buyout managers utilise financial structuring and operating expertise to improve com- pany financials in order to position the company for a strategic sale at a higher valuation.

Growth equity involves building companies with solid, proven business models that are poised for further growth due to strong underlying demand, good management, a good balance sheet and a point of difference.

Private equity has generated compelling historical returns by outperforming its listed counterparts over multiple time horizons and across geographic regions. It has also outperformed listed equity in various economic conditions and, in particular, in periods of economic stress, such as the GFC in 2008.

With private equity having generated these higher returns at lower levels of risk (as measured by return volatility) compared to listed equities over the past 20 years, there is a potential for private equity to deliver diversification benefits to investors’ portfolios, if they are able to get past the traditionally high barriers to entry. Adding even small amounts of private equity to a portfolio can potentially increase overall returns and lessen volatility.

Like a good wine, the year in which private equity investments are first entered into, the vintage, can have significant influence on the end result.

Private equity has escaped the worst of the market downturn in 2022, which for equities and bonds has been worse than the first half of 2008. But private equity tends to lag equities and bonds by one or two quarters, so it could face some short-term headwinds during the second half of 2022.

Market downturns tend to have a more muted impact on the valuations for private equity than listed equities, as private equity does not experience the same big fluctuations in company valuations. Until recently, prices for listed equities have been very high compared with company earnings, yet prices for private equity buyout deals were comparatively more reasonable and stable, and therefore more appealing than listed equity counterparts, and less likely to experience severe correction.

Private equity managers can also leverage tougher market conditions to conservatively structure deals to include stronger downside protection and significant upside participation. As with timing the market, however, trying to select the best vintage can be difficult. An investor’s ability to capitalise on these vintages relies heavily on selecting the right managers, with the right connections, to do the right deals – but this raises questions around access.

Private equity is a long-term game, and its underlying access characteristics have historically been a major barrier to entry for everyday investors and even high- net-worth individuals.

It is typically accessed through newly established “primary” funds, which invest into a portfolio of underlying companies. Investors make commitments during an initial fundraising period, with the usual minimum amount of $5 million to $10 million serving as a roadblock for many investors.

The identification, due diligence and selection of managers at the outset are paramount for a successful investment: there is a clear performance gulf between the top-quartile and median private equity funds, much more so than their listed equivalents.

Gaining access to top-quartile funds is, therefore, vital to achieving consistent performance.

But it’s not easy. Not only do the best private equity managers not need your money, in many cases they don’t even want your money – the demand for their expertise is so great that many of the top-quartile managers’ new funds are oversubscribed before they even open for investment.

Many private equity funds have a life of 10 years or more, although some investments may see some realisations after five to seven years. They are specifically structured to be illiquid.

Even high-net-worth individuals struggle to create their own sufficiently diversified private equity portfolios – a well-structured, diversified private equity program may require upwards of $100 million in capital, considering the high minimum investment to access a single fund manager.

Private equity firms with capital to deploy are able to buy distressed assets at attractive prices

Until recently, private equity has really been the domain of the uber wealthy or big institutional investors, such as the Future Fund.

But everyday investors are starting to gain access.

In 2019, Pengana Capital Group announced a partnership with the US-based GCM Grosvenor, a $US71 billion ($105 billion) private equity powerhouse, to launch the ASX-listed Pengana Private Equity Trust (PE1).

This solves the access issues, with everyday and self-managed super fund investors now able to invest in a diversified portfolio of global private equity, with low barriers to entry and daily liquidity made availa- ble through an ASX-listed investment trust structure.

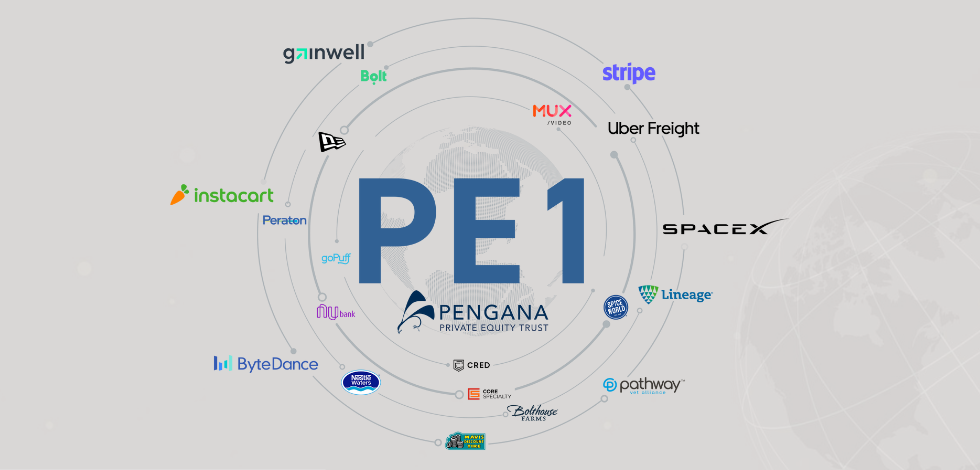

The trust offers investors a single point of entry to a global portfolio of more than 400 underlying private companies, with an expectation that this will further increase to more than 500 over time, as new primary funds are added the underlying portfolio.

The trust is further diversified through exposure to deals across economic cycles that span from 2003 to the present day, and has utilised a range of private equity strategies and implementation methods. It focuses on the middle market – companies with enterprise values of $US500 million to $US1.5 billion, and avoids investments in venture capital.

The trust recently reported a net return of 26.7% for 2021-22. Since inception to June 30, 2022, it has delivered a 13.4%pa net return on its net asset value.

More companies are choosing to remain in private hands, yet they may still require capital. They still need to refresh their shareholder base, and they need to expand their businesses, which has the potential to provide an enormous opportunity for investors who can access this part of the market.

There’s a saying in private equity circles: “private equity managers love a good recession”. Recent history has shown that while private equity has outperformed listed equity across all stages of the economic cycle, this effect is magnified during, and immediately following, recessionary periods.

Historically, private equity firms with capital to deploy are able to buy distressed and/or undervalued assets at attractive prices.

Middle-market companies are currently particularly attractive in private equity because they have a broader range of exit options, including trade sales, management buyouts or sales to other private equity funds. They don’t need to rely on initial public offerings (IPOs), which is a good thing, as IPOs have dropped off this year. The other great advantage of middle-market companies is the ability to secure favourable terms for additional rounds of venture capital raising.

Private equity has been particularly active in recession-resistant industries, such as consumer staples, healthcare and utilities, which are holding up relatively well. Continued outperformance will likely depend on targeting pockets of stability and opportunity alongside the right managers, with a focus on profitable companies in defensive and attractive industries including consumer staples, government services, IT, logistics and healthcare.

Russel Pillemer is CEO of Pengana Capital Group.

Investors are clamoring to buy into listed global technology companies – on the Nasdaq, the ASX, and other exchanges worldwide, driving valuations to all-time highs.

And then there are unlisted global technology companies, many of which have phenomenal growth prospects but are valued at much lower multiples than their public market counterparts. Unfortunately for most investors, it is impossible to invest in these unlisted companies which usually only raise money from large institutions and extremely wealthy family offices – who get to share in what is often substantial gains, when these companies are listed or sold.

Examples of market-leading, unlisted, global technology companies that are owned by PE1 include:

![]()

Instacart: the leading independent grocery delivery platform in the US and the largest single investment in the PE1 portfolio. Instacart which has had 500% volume growth over the last year, is reported to be targeting an IPO in the first half of 2021.

![]()

Stripe: a payment processing company with software that allows businesses to make and receive payments, primarily in e-commerce environments. We believe that Stripe is the globally preferred solution for both e-commerce and software as a service (SaaS) companies.

![]()

ByteDance: the second-largest internet platform in China and owner of TikTok. The company has 800 million daily average online users of its video, live streaming, and newsfeed apps, accounting for 12% of time spent online in China. Recently reported to be raising an additional US$2 billion, valuing it at circa $180 billion.

![]()

Transferwise: a payment platform launched in 2011, designed to provide its customers with the lowest possible costs on foreign currency transfers. With 8 million customers, Transferwise employs 2,200 people across 14 offices globally and processes in excess of US$5 billion of transfers per month.

![]()

Transact: a payment and campus management software platform operating in the higher education market, serving ~1,300 unique institutions and over 12 million students globally.

![]()

Nubank: a Brazilian company that is the largest Fintech in Latin America, offering credit cards, personal loans and savings accounts by smartphone without the need for physical documents and branch visits. Nubank has 23 million unique customers, equating to 14% of Brazil’s adult population.

![]()

SpaceX: an American aerospace manufacturer and space transportation services company founded in 2002 by Elon Musk, with the goal of reducing space transportation costs to enable the colonization of Mars.

![]()

Uber Freight: an UBER-for-freight-logistics app that helps carriers make hassle-free bookings and shippers tender shipments easily.

Let’s take a look at a recent example of a pre-IPO investment that Australian retail investors who hold PE1 were able to access.

![]()

Unity software is a mobile game development platform operating in a global duopoly with an increasing market share in a rapidly growing market. The Unity platform boasts 1.5 million active creators, over 3 Billion app downloads per month, with over 50% of all mobile games in the world being created using Unity’s platform.

In September of 2019 PE1 invested in Unity at a price of $22 per share. In September of 2020, Unity executed an IPO at $52 per share and is now valued at circa $95 per share (as at end of October 2020). PE1 still holds in investment in Unity which is currently worth 4.3x its entry price.

PE1 is listed on the Australian Stock Exchange (“ASX”) and therefore is accessible to investors who are able to acquire ASX listed investments.

In addition, most major investment platforms allow their investors to invest in PE1 units.

Speak to your financial advisor about an investment in PE1 or contact us directly.

Disclaimer:

Whilst PE1 has the potential to generate returns from investing pre-IPO, it is important to note the following:

Pengana Investment Management Limited (ABN 69 063 081 612, AFSL 219 462) (“Pengana”) is the issuer of units in the Pengana Private Equity Trust (ARSN 630 923 643) (“Trust”). A Product Disclosure Statement for the Trust (“PDS”) is available and can be obtained by contacting Pengana on (02) 8524 9900 or from www.pengana.com. A person who is considering investing in the Trust should obtain a copy of the PDS and should consider the PDS carefully and consult with their financial adviser to determine whether the Trust is appropriate for them before deciding whether to invest in, or to continue to hold, units in the Trust.

This report was prepared by Pengana and does not contain any investment recommendation or investment advice. None of Pengana, Grosvenor Capital Management, L.P., nor any of their related entities, directors, partners or officers guarantees the performance of, or the repayment of capital, or income invested in the Trust.

Certain statements in this report constitute Pengana’s opinions on investment related matters. While Pengana has a reasonable basis for holding these opinions these do involve known and unknown risks, uncertainties, assumptions and other important factors, many of which are beyond the control of Pengana and which may cause actual performance or outcomes to differ materially from those expressed or implied by such opinions. To the maximum extent permitted by law, Pengana disclaims any obligation to disseminate any updates or revisions to Pengana’s opinions as expressed in this report.

An investment in the Trust is subject to investment risk including a possible delay in repayment and loss of income and principal invested. Past performance is not a reliable indicator of future performance, the value of investments can go up and down.

The original article was published in firstlinks 24-March-2022, and is available HERE

The $200 billion Future Fund is not alone in its enthusiasm for private market investments. One of the most significant financial trends since the turn of the century has been the explosive growth in private markets.

Private Equity is the cornerstone of the Future Fund’s illiquid portfolio, accounting for 16.8% of total portfolio allocations, second in size only to their global listed equities portfolio (including both developed and emerging markets).

Meanwhile, Calpers, Americas largest public pension fund, has announced an intention to increase exposure to private equity and private debt from 8% to 18% as we see the acceleration of a well-established trend: Morgan Stanley says US companies (the largest market for private investments) have raised more money in private markets than in public markets each year since 2009.

The magnitude of the ongoing opportunity is still emerging, as private markets are significantly larger than public markets, according to the S&P Capital IQ database.

Companies with revenues ≥ US$15 million

Private equity refers to capital invested in companies that are not listed on public exchanges. Such investments can be made at any stage during the corporate life cycle.

The characteristics, risk, and potential return of private equity investments typically vary according to the stage at which the investment is made, with most investments being made once companies are more mature and validated:

Angel Investing is initial private funding support often backing little more than an idea and an entrepreneur.

Venture Capital is where managers actively work with early-stage or start-up investments to develop the business to raise further capital to fund commercialisation.

Growth Capital generally follows the venture capital stages as companies with viable business models and proven demand prepare for success on a larger scale. An increasing portion of growth capital funds customer acquisition.

Buyouts are the largest private equity segment. Transactions involve buying all, or a controlling stake, of a mature company with intention to improve its business and financial health, later reselling it for a profit to an interested party or conducting an IPO. Such transactions are often called leveraged buyouts as predictable future cashflows are ‘leveraged’ such that the acquisition can largely be debt financed, thereby bolstering investor returns.

Distressed funding is niche and generally involves acquiring the debt, equity or assets of a distressed business with the intention to restructure, recapitalise, and return to profitability.

Most private equity funds have an investment term of 10-12 years with only a small portion of the committed capital generally required upfront. The investments are typically made during the first five years with the realisations occurring later in the life of the fund.

Since the GFC, more companies have chosen to stay private rather than list on public exchanges as the regulatory burden for listed companies has become increasingly onerous and the funding options for unlisted businesses have improved.

Investors are attracted to private equity for:

Private equity’s lower correlation with listed equities has become more relevant as investors seek to diversify away from heightened valuations in global equities, and anaemic cash returns.

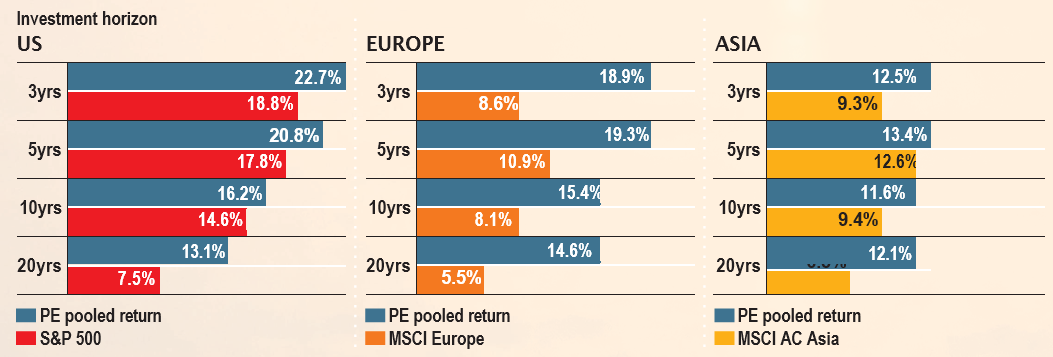

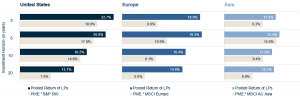

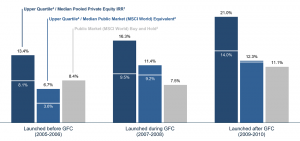

The charts below illustrates how private equity has outperformed listed equity across time horizons and geographic regions. There is also greater variation in performance among managers when compared with listed equity funds, meaning investors who commit to top-tier private equity managers can expect to capture much greater levels of outperformance than the averaged-out returns displayed below.

1 The Public Market Equivalent (“PME”) concept allows investors to compare the performance of private equity and other private markets investments (Private Equity) to other types of investments, such as public market indices (Public Equity). The methodology assumes buying and selling a given index according to the timing and size of the cash flows between the investor and the private investment. Performing this comparison requires the construction of a hypothetical investment fund that mimics private equity cash flows. This hypothetical fund purchases and sells shares of the index at the same time the private equity vehicle calls and distributes cash.

Sources: MSCI, S&P and BURGISS

The benefits of investing in private equity have traditionally accrued to institutional, wholesale, and ultra-high net worth investors who are better placed to manage the traditional complexities associated with investments in the asset class.

This changed in 2019, when Pengana Capital Group listed the Pengana Private Equity Trust (ASX:PE1), a listed private equity vehicle specifically designed to enable everyday retail investors to overcome the many barriers in accessing private equity.

The LIC structure is most appropriate for listed private equity because it allows an investment manager to unitise illiquid underlying investments into shares and list on the market. This structure solves several challenges of private equity investing, including:

High barriers to entry: Private equity fundraisings are extremely exclusive with significant excess demand for top managers; PE1 partnered with US-based GCM Grosvenor to leverage existing access via a well-established private equity manager with long-standing relationships, which provides exposure to these difficult-to-access private equity opportunities.

Capital constraints and high minimum investment requirements: Typical private equity funds may require a minimum of $5-10 million for a single investment. PE1 provides access to a truly diversified portfolio of private equity investments across underlying investment managers, economic conditions, vintages, geographies, sectors, and strategies (PE1 has exposure to nearly 400 underlying companies).

Highly illiquid: Existing private equity vehicles lack liquidity with an average 10-year capital lock up. But the LIC structure means PE1 investors have daily liquidity on the ASX.

Complex cash-flow management: Traditional private equity funds require capital to be contributed on a drawdown basis and exhibit lumpy returns as investments are realised and funds wound up. Yet the listed investment trust structure allows for internally managed cashflows, with drawdowns and distributions managed by the portfolio manager. Distributions are further reinvested to gain new private equity exposures.

No regular distributions: Regular distributions are a challenge for traditional unlisted private equity, yet PE1 can target a 4% p.a. distribution paid semi-annually.

In its Global Private Equity Report 2021, Bain and Company shows that one of private equity’s enduring strengths is its ability to thrive during periods of economic disruption with downturns historically providing excellent investment opportunities. This is particularly evident when assessing the returns (IRRs in the 17 – 21% range) of funds established in 2002 and 2009 following the last economic downturns.

All current evidence indicates inflation is likely to remain elevated, with potential for huge spikes following Putin’s invasion of Ukraine. Global interest rates could march steadily higher. This will put pressure on businesses with excessive leverage and valuations.

In the private markets, these characteristics are typically associated with the very large funds and mega transactions where the deal terms reflect the intense competition to deploy vast amounts of capital. Middle market transactions are typically completed with lower levels of leverage, and at lower valuations, which should provide a measure of additional protection in a rising rate environment.

The recent inflation shock presents a unique opportunity for private equity managers to offer solutions to high quality businesses that require continued financing and structuring them to include strong downside protection for investors while preserving meaningful upside.

Russel Pillemer is co-founder and Chief Executive Officer of Pengana Capital Group, which operates the Pengana Private Equity Trust (ASX: PE1). This article is general information and does not consider the circumstances of any investor.